If you think this article is about a fantasy saga series that was popular in the past decade, no, it is not. Rather, the two kings in this article had lived harmoniously together for the past ten years and thank goodness no war had erupted between them (except probably the “war” in your mind on who to invest on).

The two mentioned “kings” are actually two REITs, namely Frasers Centrepoint Trust (FCT), the “north”, and Mapletree Commercial Trust (MCT), the “south”. Why they were given these monikers was because of the location of their respective properties (directly owned, indirectly owned and/or potential) in the geographical regions of Singapore. If you take out their annual reports and read up on their assets, the geographical concentration was obvious.

In this post, we shall take a brief look on these two REITs.

FCT: The Northern King

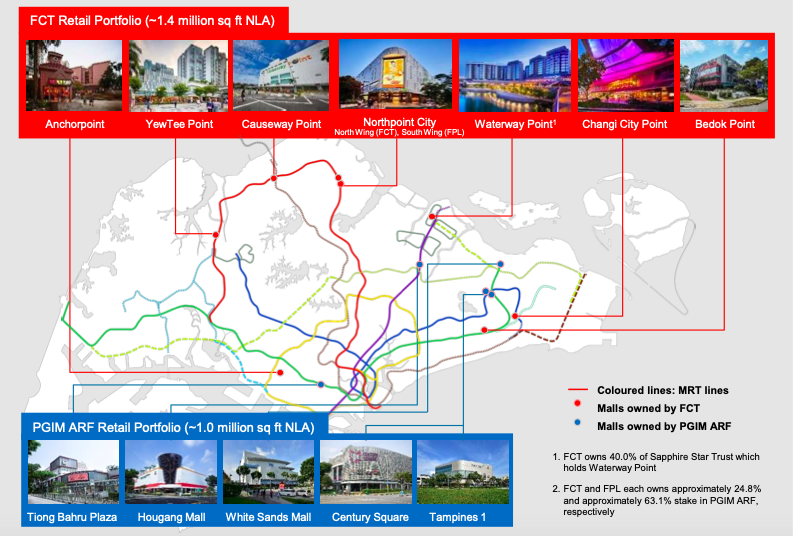

Seasoned REIT investors would have known about FCT; a retail REIT that included Northpoint, Causeway Point, Changi City Point etc. as part of its portfolio. On top of these, there are also indirect and minority stakes in other malls such as Waterway Point, Century Square, White Sands Mall, etc. Its only international holdings are a 31.15% stake in Malaysia-listed retail Hektar REIT.

From Figure 1 (below), FCT’s malls are like everywhere, but the key area is in the north, where it held a near-captive share on the category of heartland malls in the estates of Woodlands, Yishun and Sembawang. Causeway Point and Northpoint themselves in FY2019 had a combined footfall of 83.8 million1, a very high number indeed.

Fig.1 – Locations of FCT-related malls2.

Besides being dominant in the north, most of FCT’s malls are situated just next to MRT stations and this is a huge benefit (PS: for more information on the analysis of retail REITs based on location, you can read up my post here). These factors had contributed to the premium of FCT, which most of the time was trading above its NAV.

FCT’s sponsor, Frasers Property Limited (FPL), is no stranger to the real estate business; it has multiple properties that spans across sectors like hospitality, office, logistics, etc. and in several countries like Australia, China, Singapore, etc. Retail wise in Singapore, Centrepoint and Northpoint City’s South Wing are under FPL and there may be a possibility of them being brought into the FCT family.

MCT: The Southern King

All of MCT’s six properties are situated in the southern part of Singapore; Vivocity, Mapletree Business City (MBC) I, MBC II, PSA Building, Mapletree Anson and Bank of America Merrill Lynch Harbourfront (MLHF) (see Figure 2 below). Unlike FCT which is mainly retail, MCT has a sizable office and business park component.

Fig.2 – MCT properties3.

The crown jewel of MCT is its retail asset Vivocity and it contributed to about 42% of the REIT’s net property income ($158.7m/$377.9m)4 in FY 19/20. MCT’s office and business park properties deserved a mention as well. Their top tenant, Google Asia Pacific Pte Ltd, is situated at MBC and contributes 10.1% of the gross rental income for MCT.

MCT’s sponsor, Mapletree, is a leading real estate development and management company, and they have a slew of properties that could be injected into MCT5. The said properties include Harbourfront Centre, the neighbouring Harbourfront Towers One and Two, St James Power Station, etc., and they are literally next to the Vivocity and MLHF. Hence, if they are brought into MCT, their kingship for the south is undisputable, even more so with the development of the Greater Southern Waterfront to come.

The COVID-19 Impact

When mandatory measures to curb the spread of COVID-19 was declared in early April 2020, retail properties took a big hit with the suspension of non-essential businesses, effectively reducing the footfall to malls. Though after Phase 2, shopping centres are starting to see crowds coming back, but it may not reach its previous peaks since crowd controls are in place. Judging from my view of our local culture, malls (especially heartland ones) are still very much part of our lives and in my opinion, they are here to stay.

Office properties may be affected, too, in the future, as their relevance is being questioned with the increasing trend of telecommuting, or better known now as “work from home” (WFH). No doubt some businesses and sectors still require offices, but there may be a shift to a new norm with regards to work styles and locations. Only time can tell on how this aspect will develop.

Addressing The Elephant In The Room

Very much was written on these two REITs, but if you are observant enough, I may be missing the proverbial “elephant in the room”, and now I am going to address it.

Yes, that elephant would be the merger of CapitaLand Mall Trust and CapitaLand Commercial Trust. By their properties combined, they could be classified as the third king with the title “king of everywhere else in Singapore”. They also have malls right next to MRT stations and office spaces in the heart of the Central Business District. The upcoming combined CapitaLand REIT is also a good consideration, but maybe we will leave it for another post.

The Bedokian is vested in FCT.

1 – Frasers Centrepoint Trust. Fact Sheet. 19 Nov 2019. https://www.frasersproperty.com/reits/fct/-/media/feature/project/frasers_fct/reports-and-presentations/fct_factsheet_19_nov_2019.pdf (accessed 14 Aug 2020)

2 – Frasers Centrepoint Trust. Financial Results Presentation for the Second Quarter ended 31 March 2020. 23 Apr 2020. https://fct.frasersproperty.com/newsroom/20200423_073633_J69U_U8ZS0QDNEFGPSGRK.3.pdf (accessed 14 Aug 2020)

3, 4 – MCT Annual Report 2019/2020. https://www.mapletreecommercialtrust.com/services/view_file.aspx?f={6DA58A79-7E05-4128-A7B0-9CCAEF92B959} (accessed 14 Aug 2020)

5 – Mapletree Commercial Trust Investor Presentation. 22 Jun 2020. https://www.mapletreecommercialtrust.com/services/download_file.aspx?f={24EE051C-C206-4DFC-9153-A1BF12CD0E1C} (accessed 14 Aug 2020)

No comments:

Post a Comment